The rules of money change when you stop working.

During your working years the goal was accumulation – grow as much as possible, ride out the market, and let time do the heavy lifting. A market crash was an inconvenience. You had years to recover.

In retirement the equation flips entirely.

Now you are withdrawing money while the market moves. And that changes everything – because a market crash in the first few years of retirement is not an inconvenience. It is a permanent threat to how long your money lasts.

This is why the same strategies that built your wealth cannot be the ones that protect it.

The Fear Nobody Talks About – Running Out of Money

Market crashes get the headlines. But for most women approaching retirement, the single greatest fear is not a crash.

It is outliving their money.

According to Allianz Life, 64% of Americans worry more about running out of money than about death itself. And that fear has real consequences. Women who carry it often underspend dramatically – living on just 2% of their savings per year – depriving themselves of the retirement they worked decades to build.

The problem is not discipline. The problem is structure. When your income is not guaranteed, every withdrawal feels like a risk. Every market drop feels like a threat. And the joy of retirement quietly drains away into anxiety.

The solution is not more willpower. It is a different kind of financial floor.

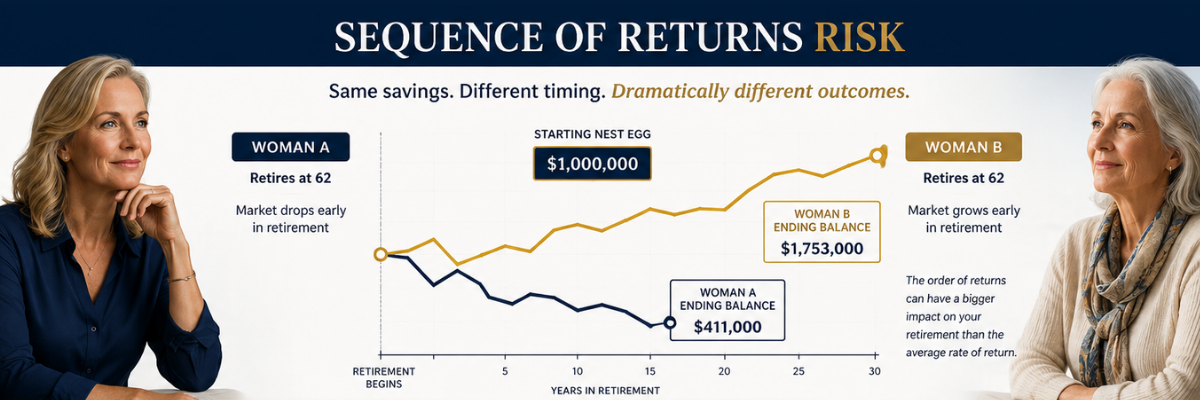

The Sequence of Returns Risk — Why Timing Matters More Than You Think

Here is something most financial advisors do not explain clearly: two people can retire with identical savings, identical withdrawal amounts, and identical average market returns — and end up with completely different outcomes.

The difference is timing.

Person A retires the year before a 20% market crash. Her account drops from $1,000,000 to $800,000. She withdraws $40,000 to live on. Now her balance is $760,000 — and every future withdrawal comes from a smaller base, during a market that is trying to recover. Her money runs out decades before she does.

Person B retires the year after that same crash, during a bull market. Her withdrawals come from a rising balance. Her money lasts dramatically longer.

Same math. Completely different life.

This is called Sequence of Returns Risk — and it is the silent killer of retirement income plans. The timing of market returns, not just the average, determines whether your money lasts.

The only reliable way to remove this risk entirely is to have income that does not depend on the market at all.

What a Fixed Indexed Annuity Actually Does

A Fixed Indexed Annuity (FIA) is one of the most misunderstood financial tools available — and one of the most powerful for women in or approaching retirement.

Here is what it actually does in plain language:

When the market goes up, your account is credited with a portion of those gains — determined by a participation rate or cap set by the carrier. You benefit from market growth.

When the market goes down, your account stays exactly where it is. You lose nothing. Zero is your floor.

This is not a gimmick. It is a contractual guarantee backed by heavily regulated insurance carriers required by law to hold dollar-for-dollar reserves. We only work with A-rated carriers with long histories of financial stability.

The result: you participate in market growth on the way up and are completely protected from market loss on the way down. Your principal is never at risk.

And in 2024 alone, Americans placed a record $434.1 billion into annuities. That is not a trend. That is a fundamental shift in how people are building retirement security.

The Income You Cannot Outlive

Beyond principal protection, a properly structured Fixed Indexed Annuity creates something most people thought was gone forever — a guaranteed income stream you cannot outlive.

Think of it as your personal pension.

Through an income rider, your FIA generates a guaranteed monthly or annual income that continues for as long as you live — regardless of what the market does and regardless of how long that turns out to be.

This is what changes everything for a woman in retirement. When a guaranteed income floor covers your essential expenses — housing, food, utilities, healthcare — you are no longer afraid to spend. You are no longer living on 2% of your savings. You are living.

The Tax Traps Most Women Don’t See Coming

Here is the truth about retirement taxes: if you don’t have a plan, the government has one for you. And their plan was not designed with your best interest in mind.

Here is the truth about retirement taxes: if you don’t have a plan, the government has one for you. And their plan was not designed with your best interest in mind.

Failing to plan for taxes in retirement is one of the most expensive mistakes I see – and it is entirely preventable, if you’re “in the know”.

Two hidden tax traps catch most retirees off guard:

Social Security Taxation. Most women are shocked to learn that up to 85% of their Social Security benefits can be subject to federal income tax – depending on their total income. This is not a rumor. It is the tax code. And most people never plan for it.

Required Minimum Distributions. If your money sits in a traditional IRA or 401k, the IRS has a silent partnership in your account. They intend to collect their cut. Starting at age 73 (or later, depending on your birthdate), the IRS requires you to take minimum distributions from tax-deferred accounts – whether you need the income or not. Fail to take them and you face a 25% excise tax penalty on the amount you should have withdrawn.

A Fixed Indexed Annuity used strategically within a holistic retirement income plan can help manage both of these traps — providing tax-deferred growth, creating tax-efficient income streams, and in some cases helping reduce the provisional income that triggers Social Security taxation.

Modern FIAs are also RMD-friendly by design. Carriers automatically calculate the exact RMD amount and distribute it accordingly – no surrender penalties on required distributions.

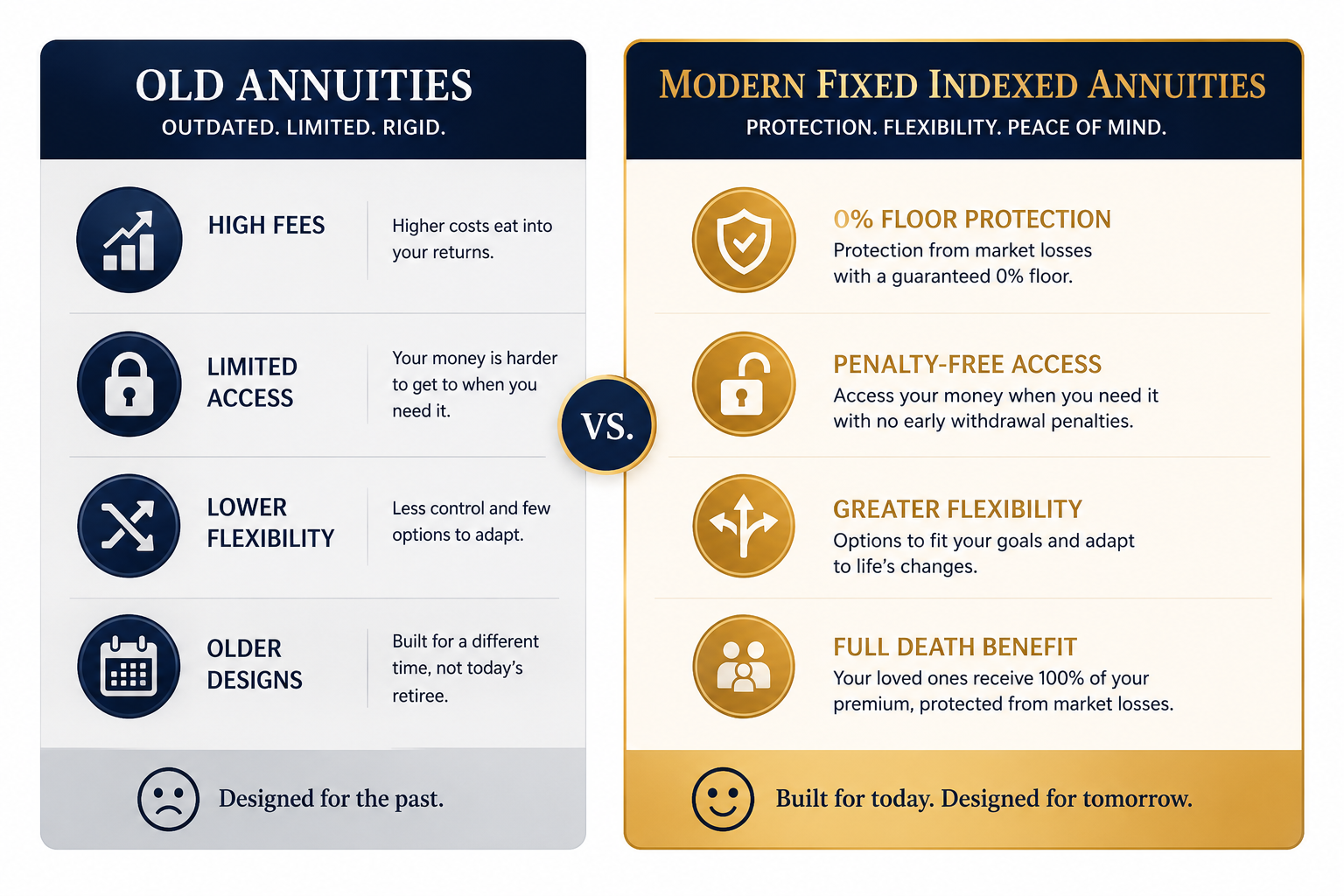

Modern FIAs vs Old Variable Annuities — They Are Not the Same Product

If someone once told you annuities are bad — they were probably talking about old variable annuities. And they were right.

Old variable annuities had high fees of 3-4% or more, direct market exposure that left your principal vulnerable, life-only payout structures that kept your money if you died early, and locked-up access with no liquidity.

Modern Fixed Indexed Annuities are a fundamentally different product:

Zero fees on most products. Principal protection with a 0% floor. Full death benefit to your named beneficiaries — whatever remains passes directly to them, avoiding probate. 10% penalty-free annual access starting in year one. Liquidity waivers for nursing home care or terminal illness.

These are not the annuities of your parents’ generation. They are built for how people actually need to live in retirement.

Is a Fixed Indexed Annuity Right for You?

A Fixed Indexed Annuity is right for you if:

— You want to protect your principal and guarantee you cannot lose money to market crashes — You want growth potential without direct market exposure — You want income you cannot outlive — You want to lower your taxes in retirement — You want to leave something to your beneficiaries

A Fixed Indexed Annuity may not be right for you if:

— You want crypto-style 40% returns and need 100% liquid access to your entire portfolio tomorrow

If you already have an annuity — that is perfectly fine. I offer a no-pressure, objective review of your current contract. If it is the right product for you, I will tell you to keep it. If a modern product offers better growth caps or income riders, I will show you the math.

Our recommendation is always driven by the objective math behind your specific situation — not a sales quota.

What a Retirement Strategy Session Looks Like

This is a working session. Not a pitch.

Before our session, I ask you to complete quick paperwork — forms that take 15 to 20 minutes and give me what I need to build your specific picture.

In the session, we review your current income trajectory, identify your income gaps and tax exposures, and look at the objective math behind your situation. I show you what your retirement actually looks like under different scenarios — and where the vulnerabilities are.

Then we build a strategy around your specific needs.

If a Fixed Indexed Annuity is part of the right solution, I work with an independent brokerage — meaning I am not tied to any single carrier. I shop the entire market to find the product that fits your specific needs. Once we agree on a strategy, the transfer process typically takes two to four weeks. I manage the entire process end to end.

If your current strategy is already solid, I will tell you that too.

Ready to start that conversation? Schedule a Clarity Call — no pressure, no rush, just clarity.

You Have Worked Too Hard to Leave This to Chance

Security is not a feeling. It is a structure.

And a woman who knows who she is does not rush the biggest financial decisions of her life — including the ones that determine whether her money outlasts her.

When you are ready to look at the objective math behind your retirement picture — I am here.

Schedule a Retirement Strategy Session

No pressure. No rush. Just clarity.

Elizabeth Rose | Retirement Strategies & Annuities Strategist NPN# 19058858 | Multi-State Licensed

This page is for educational purposes only and does not constitute financial advice or a solicitation to purchase any financial product. Annuity products vary by carrier, state, and individual qualification. Results are not guaranteed. Please consult with a licensed professional regarding your specific situation.